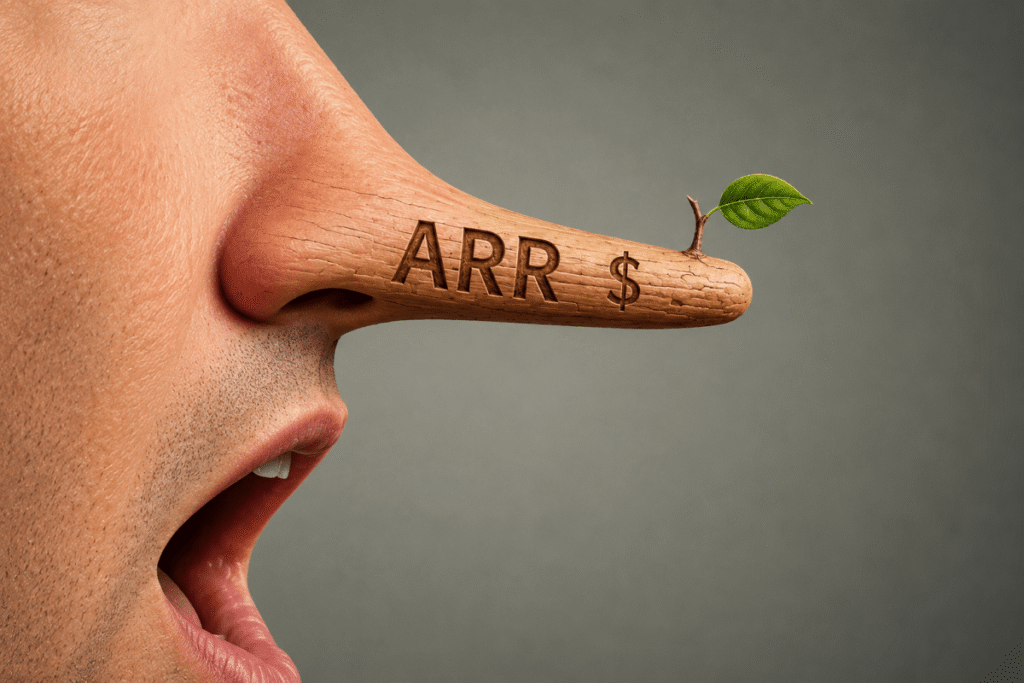

The AI Revenue Mirage: How Startups and VCs are Gaming the ARR Metric

Table of Contents

The Battle Over the Balance Sheet

Last month, Scott Stevenson, co-founder and CEO of the legal AI startup Spellbook, ignited a firestorm across X (formerly Twitter) by calling out what he described as a “huge scam” permeating the AI startup ecosystem. His target wasn’t a specific product or a failed pivot, but rather the way companies are reporting their financial health to the public.

Stevenson alleged that a growing number of AI startups are intentionally inflating their Annual Recurring Revenue (ARR) figures—a cornerstone metric for SaaS valuations—with the tacit approval of some of the world’s largest venture capital funds. According to Stevenson, these inflated numbers are being fed to journalists to secure glowing PR coverage and drive up valuations in an already overheated market.

While the claim initially appeared as a social media outburst, it resonated deeply within the founder community. Jack Newton, CEO of legal tech firm Clio, noted that the conversation brought a necessary level of scrutiny to the topic, echoing sentiments that the current reporting standards for AI revenue are, at best, inconsistent.

The CARR Shell Game

To understand the “scam,” one must look at the difference between ARR and CARR. Traditionally, ARR represents the value of the recurring revenue components of a company’s term subscriptions. It is a snapshot of committed, active revenue. However, a pervasive trend has emerged where startups substitute CARR—Contracted Annual Recurring Revenue—and simply label it as ARR in public statements.

The distinction is critical. CARR includes revenue from signed contracts where the customer has not yet been onboarded or the product has not been deployed. In the world of enterprise AI, where implementation can be a grueling, months-long process, CARR is a “squishy” metric. It assumes that every signed contract will eventually go live and be paid in full.

One investor, speaking on the condition of anonymity, confirmed that reporting CARR as ARR has become a survival mechanism in competitive categories. “When one startup does it in a category, it is hard not to do it yourself just to keep up,” the investor admitted.

The risk is that a significant portion of CARR often never materializes. If a deployment fails or a client decides to pivot during the onboarding phase, that projected revenue vanishes. Yet, for the purposes of a press release or a funding round, that money is often counted as if it were already in the bank.

Institutional Blind Spots

The inflation isn’t always a clandestine effort by founders; in many cases, it appears the board of directors and VC backers are complicit. One former employee of a high-profile startup revealed that their company routinely counted year-long free pilots as ARR. According to the source, the board—including a partner from a top-tier VC fund—was fully aware that the revenue was being counted before the customer had actually paid a dime, despite the clear possibility that the customer could cancel before the pilot ended.

In other instances, the gap is smaller but still telling. One source described a company claiming $50 million in ARR in marketing materials while internal books showed $42 million. In the fast-paced environment of AI growth, such a discrepancy is often dismissed by investors as a “rounding error” that the company will simply grow into over the next quarter.

The problem is exacerbated by another common confusion: the “annualized run-rate.” Unlike traditional ARR, which is based on contracted value, a run-rate simply takes the previous month’s revenue and multiplies it by 12. If a startup has a single massive spike in one month, their reported “ARR” can skyrocket overnight, creating a facade of exponential growth that doesn’t reflect a stable, recurring customer base.

A Lack of Standardized Audits

The reason these discrepancies persist is that ARR is not a GAAP (Generally Accepted Accounting Principles) metric. Because accountants focus on historical, collected revenue rather than future projections, ARR does not undergo the same rigorous auditing process as a standard income statement. This creates a gray area where “creative accounting” can thrive, allowing startups to present a version of their growth that looks more appealing to the market than the reality on the ledger.