Jet Fuel Spikes and Gas Hikes: How the Iran Conflict is Rewiring US Energy Costs

Table of Contents

The Pump Price Shock

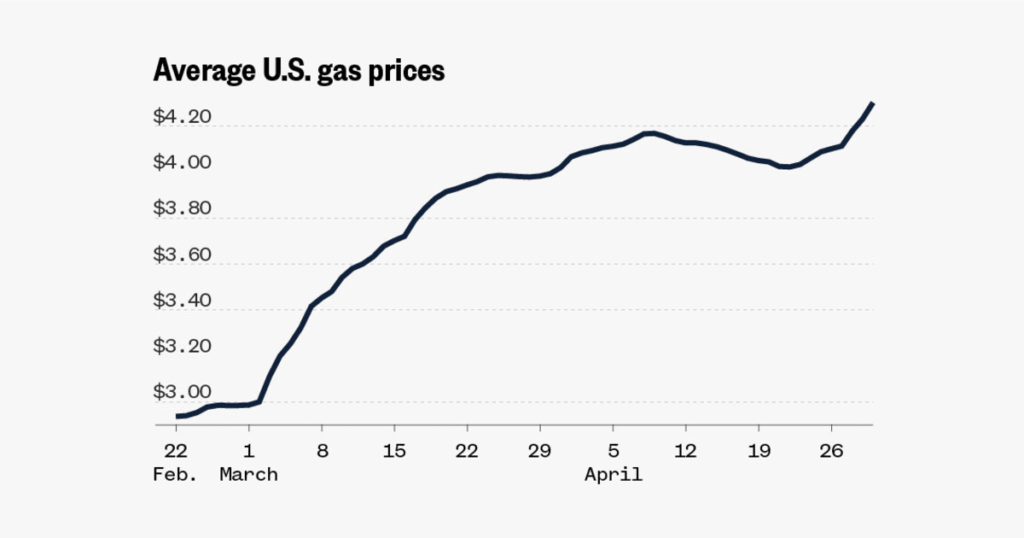

The national average for a gallon of gas in the United States has crossed the $4.50 threshold, marking the highest level of the year. According to the latest data from motor club AAA, prices have surged by roughly 50% since the onset of military operations involving the U.S. and Israel against Iran. This spike isn’t just a statistical anomaly; it is a direct reflection of a tightening global oil supply and the volatility of a geopolitical flashpoint that continues to destabilize energy markets.

For American households, the increase is visceral. In many regions, the cost of commuting has risen by more than a dollar per gallon since the conflict began. While the impact is felt nationwide, the geography of the surge is uneven. West Coast and Pacific markets are bearing the brunt of the volatility, with California prices eclipsing $6 per gallon—the highest in the country. Other states, including Alaska, Hawaii, Illinois, Nevada, Oregon, and Washington, are hovering near the $5 mark.

Beyond the Passenger Car

The crisis extends far beyond the residential gas station. The surge in crude oil prices has triggered a corresponding spike in jet fuel costs, creating a ripple effect across the aviation industry. Airlines, facing unsustainable operational overhead, have begun aggressively raising airfares to compensate for fuel volatility.

The most severe casualty of this trend has been Spirit Airlines. The ultra-low-cost carrier, already struggling with a fragile balance sheet and a shift in consumer travel patterns, has been forced to shutter operations. Spirit’s collapse serves as a canary in the coal mine for the aviation sector, demonstrating that for some carriers, the current cost of fuel is simply an insurmountable barrier to entry.

Market Volatility and the Ceasefire Tease

The behavior of oil prices over the last several months has been characterized by extreme “see-sawing.” Markets initially reacted to ceasefire announcements with sharp declines, leading some analysts to predict that prices would begin a steady descent in April. For a few weeks, that seemed to be the case as gradual declines took hold.

However, those gains were short-lived. As ceasefire extensions remained precarious and the threat of renewed hostilities persisted, prices shot back up to new highs. This pattern suggests that the market is currently trading on sentiment and geopolitical headlines rather than traditional supply-and-demand fundamentals. Every announcement of a truce provides a brief relief valve, only for the pressure to build again as the underlying conflict remains unresolved.

The Regional Divide

Data indicates a stark contrast in how different parts of the U.S. are experiencing this energy crisis. While the coasts are seeing record-breaking numbers, states in the center of the country continue to pay the least. This disparity is largely driven by proximity to refining hubs and different state-level tax structures, but the national average continues to be dragged upward by the extreme costs in California and the Northwest.

As the U.S. and Israel continue their strategic maneuvers in the region, the energy sector remains the most sensitive barometer of the conflict’s duration. Until a stable, long-term diplomatic resolution is reached, the volatility at the pump—and in the skies—is likely to persist.